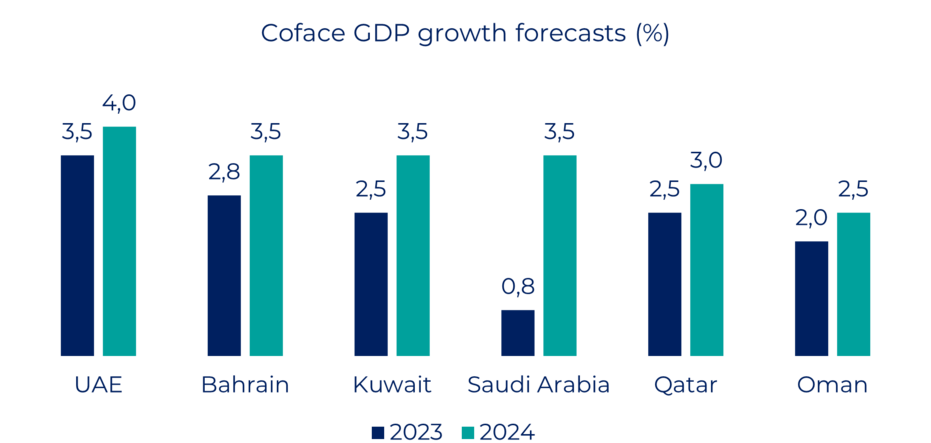

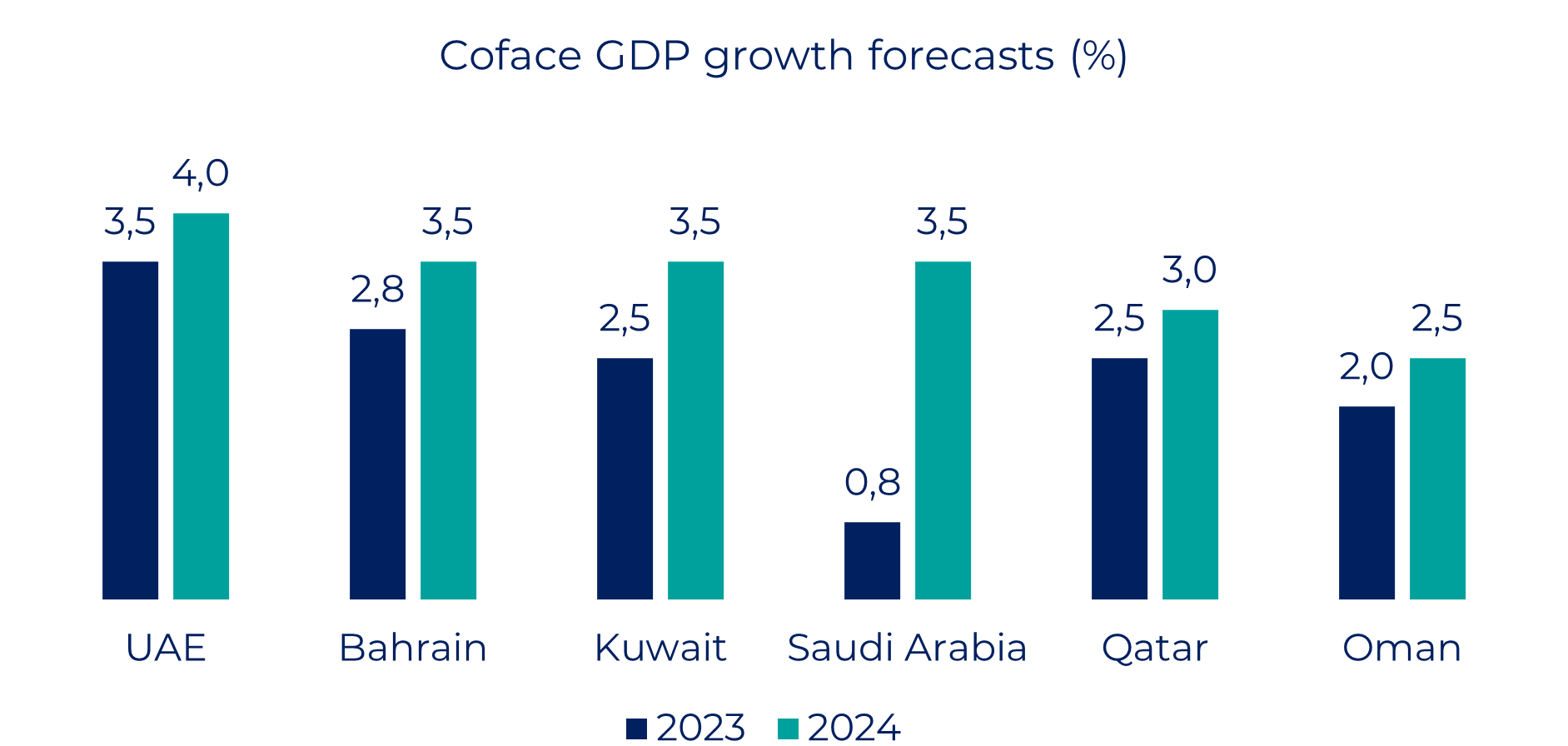

After a slowdown in 2023 mainly due to lower energy production and prices, 2024 is expected to be a year of higher economic growth for the Gulf Cooperation Council (GCC) countries as, after several months of pessimism about global oil demand, prices have been on the rise since summer. But all countries are not equal…

The favourable economic environment should not conceal the structural vulnerabilities of some economies: Bahrain and Oman, the weakest links in terms of public accounts

After several months of pessimism about global oil demand, prices started to rise following the announcement by Russia and, above all, Saudi Arabia, of the extension of their production cuts until the end of the year. However, this slight increase in oil prices will not benefit all of these countries equally.

Due to their high level of public debt, structural fiscal weaknesses and more limited natural resources compared with other countries in the region, Bahrain and Oman will must remain vigilant. Bahrain should continue recording the highest public debt-to-GDP ratio in the region with 125% in 2023. Given the high level of its fiscal breakeven oil price, estimated at around USD 125 per barrel for 2023, the authorities have begun to consider measures to limit a further widening of the budget deficit. Despite recurrent current account surpluses, the large fiscal deficit, and the need to preserve the currency peg, weigh on Bahrain’s foreign exchange reserves. While reserves covering three months of imports are conventionally regarded as the minimum adequate level, Bahrein’s reserves would only cover 1.5 months of imports in 2023.

Oman’s debt dynamics seem more balanced but it suffers from structural fiscal weaknesses as well, mainly on the back of limited natural resources. Since the fall in oil prices in 2015 and 2016, Oman had been continuously recording twin deficits (both current and fiscal accounts).

Saudi Arabia and the UAE, much less vulnerable, usually come to help

Saudi Arabia, Kuwait and the United Arab Emirates usually come to help in case of emergencies when funding is in short supply.

These 3 countries announced a USD 10 billion aid package to Bahrain in 2018, after providing USD 20 billion to both Oman and Bahrain in 2011, underlying the strategic and economic alliances among those countries. These funds have mostly supported the reduction of fiscal deficits in Oman and Bahrain and mitigated the negative effects of the fiscal consolidation programs. Another aim of this fiscal cooperation is to align all the GCC economies around similar regional initiatives through the introduction of some fiscal reforms.

Different financial situations but (virtually) the same monetary policies

These different structures within the GCC economies indicate that, while these countries have formed an economic and financial alliance, their financial situations are unequal. However, regarding monetary issues, they have very similar structures: their currencies are pegged to the US dollar, except for Kuwait that has a currency peg against an undisclosed currency basket. In line with the Fed’s future policy moves, we expect GCC central banks to hold their policy rates until the Fed decides to begin its rate cut cycle.

Fierce competition in the sectors targeted by diversification efforts

Although they still heavily depend on the oil sector, GCC countries implemented economic diversification plans following the drop in oil prices between 2014 and 2016. While the UAE have been at the forefront of economic diversification, Saudi Arabia has announced substantial investments in recent years. As these two countries, but also Qatar and, to a lesser extent, Oman, are targeting almost the same sectors (construction, tourism, finance), the key risk resides in the creation of intra-competition within the region. Additionally, the main financing sources for these diversification strategies are based on oil revenues. Considering these two factors, economic diversification strategies, while feasible, may not yield the desired results.